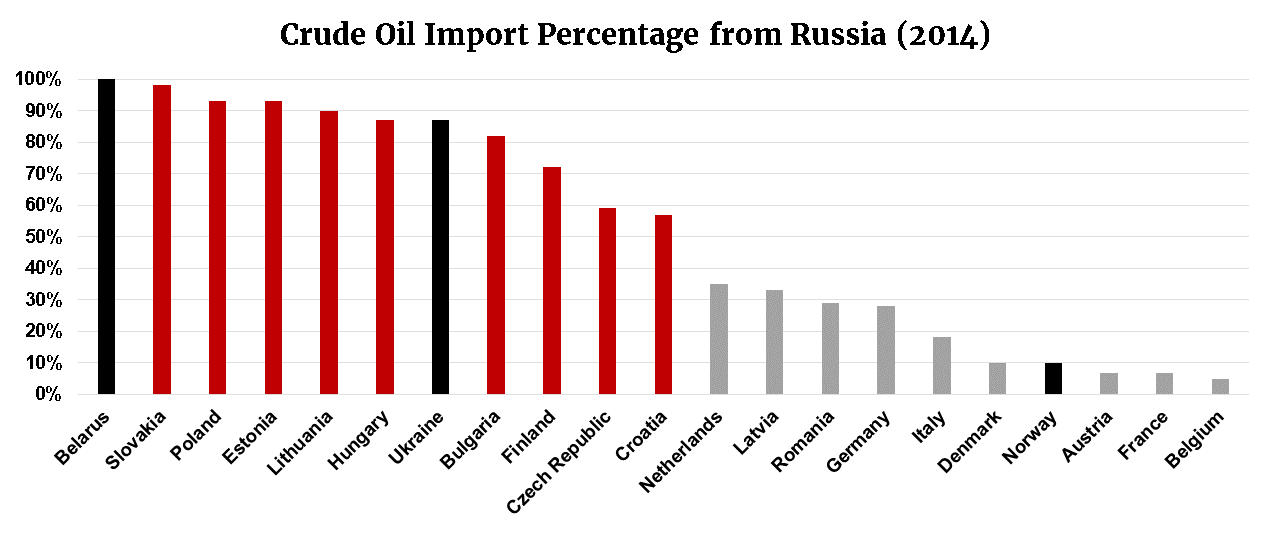

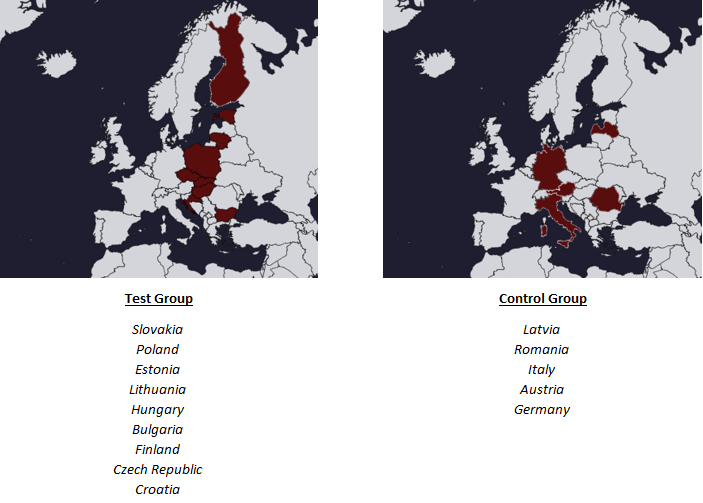

Is it possible that the 2014 U.S. and EU-led Russian sanctions could have significantly affected the economic performance of Central Eastern European nations? If one of a nation’s biggest trade partners has an economy hampered by sanctions, it seems logical that costs could be passed onto end users. Our Fulbright intern colleague investigates this possibility within energy markets, specifically regarding changes in gasoline prices. This iteration of his research finds no significant relationship between the implementation of Russian sanctions and price increases for regional nations that import more than 50% of their crude oil from Russia.

Over three years have passed now since the United States and the European Union introduced the first round of economic sanctions upon the Russian Federation for their alleged role in the annexation/invasion of the Crimean Peninsula.

The renewal of these economic sanctions each year has corresponded with an increase in the quantity of voices in Central and Eastern Europe (CEE) nations which argue that these sanctions are harmful for their domestic economies. Such a reasoning is logical, considering the geographical and historical trade ties that have bound CEE nations and Russia. For my research, I felt this was an under-scrutinized topic which deserved further exploration. Are Western sanctions economically affecting CEE nations in some significant way? Are the voices spreading this message correct?

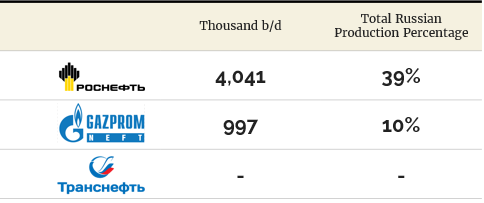

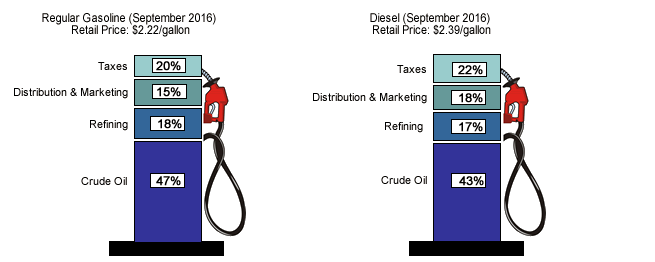

To review, U.S. and EU sanctions target particular Russian individuals and three core Russian industries – energy, banking & finance, and defense. Russia responded to these sanctions with counter-sanctions of their own, targeting certain American and European politicians and creating a de facto embargo on European agricultural imports. For this work, I chose to focus on the economic sector most vital for the health of the Russian economy and their greatest export to the EU – energy. Within the energy sector, Rosneft, Transneft, and Gazprom Neft are the three specific organizations designated by EU sanctions. Sanctions restrict the ability to trade debt and equity products of Rosneft, Transneft, and Gazprom Neft and do not allow them to raise capital in Western markets via products that exceed 30 days in maturity. Reduced financial flexibility should result in higher operational costs for these firms, which may be passed onto end (e.g. CEE) consumers. Rosneft, Gazprom Neft, and Transneft are all integrated into a variety of energy product value chains. So, to narrow things down further, I chose to focus on gasoline, a product that affects the daily life of almost everyone around the globe.

Now, to be clear, Rosneft, Transneft and Gazprom Neft were targeted for a reason. These are massive companies that are vital contributors to the Russian energy sector.